The Bank of Jamaica (BOJ) raised its policy rate by 100 basis points to 1.50 percent in the first policy tightening since the current monetary policy framework and rate was introduced in July 2017.

It is also BOJ's first change of its policy rate since the rate was lowered to the historic low of 0.50 percent in August 2019 as a decade-long monetary easing cycle came to an end as inflation sustainably settled within the bank's target range of 4.0 to 6.0 percent.

"Summary of

Monetary Policy Discussion and Decision

September 2021

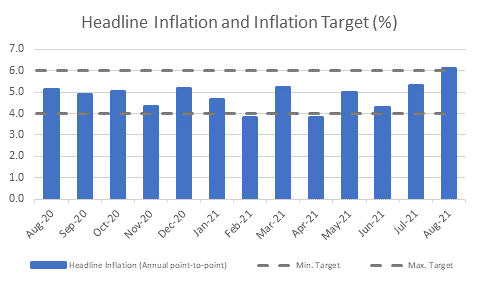

Bank of Jamaica’s Monetary Policy Committee (“MPC/the Committee”) sets monetary policy to meet the inflation target of 4.0 per cent – 6.0 per cent, as outlined by the Minister of Finance in April 2021.

At its meetings on 28 and 29 September 2021, the MPC noted that inflation had breached the upper limit of the Bank’s target range in August and that the risks of inflation continuing to breach the target over the next year have intensified. The recent significant increases in international commodity prices and shipping costs have had a stronger than expected pass through to local prices. These increases have contributed to a further rise in inflation expectations, which were already elevated. Consumers will also be faced with higher prices for agricultural commodities as a result of the recent passage of tropical storms Grace and Ida in August 2021, which may also contribute to a worsening of inflation expectations.

In order to limit the second-round effects of the above noted shocks, which could then cause inflation to breach the upper limit of the Bank’s target over a protracted period, the MPC agreed to reduce its level of monetary policy accommodation, by increasing the policy rate by 100 bps to 1.50 per cent. This is against a background of an extended period of very accommodative monetary policy with the policy rate at a historic low of 0.5 per cent since August 2019. Accompanying this rate increase, the Committee decided to continue implementing measures to contain Jamaican dollar liquidity expansion. The Committee also reiterated that, while the Bank does not target any specific level of the exchange rate, Bank of Jamaica will continue to ensure that further movements in the exchange rate do not threaten the inflation target.

Finally, consistent with meeting its inflation target sustainably in the medium term, the MPC agreed to continue increasing the Bank’s policy rate (and by extension raising real interest rates, which are currently significantly negative) and maintaining or intensifying the accompanying measures. This position is subject to inflation and other macroeconomic data evolving as projected.

The following considerations informed the Committee’s decisions:

- The annual point-to-point inflation rate at August 2021 was 6.1 per cent, above the July 2021 outturn of 5.3 per cent and the Bank’s target range (see chart below). The acceleration in inflation primarily reflected the effects of higher prices for food (both processed and agricultural), meals consumed away from home and selected services such as education and transport. This breach of the inflation target occurred earlier than expected and the MPC will be writing to the Minister of Finance & Public Service to explain the causes of the breach, the measures that have been taken by the Bank to restore inflation to the target range and the short-term outlook for inflation.

- The private sector’s expectation of inflation remains elevated and continues to increase. In the latest survey as at July 2021, respondents indicated that they expect inflation over the ensuing twelve months to be 7.4 per cent, significantly above the Bank’s inflation target and above the expectations reported in the previous three surveys.

- Inflation was projected in August 2021 to average 5½ to 6½ per cent over the next two years, which was higher when compared to the average inflation rate of 5.0 per cent over the past two years. Inflation was projected to breach the upper limit of the Bank’s target range over the next twelve months. Conditional on the gradual tightening of monetary conditions, inflation was projected to remain at 5.0 per cent over the medium term.

The inflation forecast for the next two years anticipated a gradual rise in core inflation, supported by the lagged impact of higher international commodity and shipping prices and a recovery in domestic demand. The recovery in domestic demand conditions was expected to be driven mainly by external demand. The outlook for inflation also contemplated the effects of one-off adjustments in selected regulated prices as well as further increases in house rental rates. In addition, inflation was projected to be affected by the lagged and second round impact of energy prices. While international commodity and logistics prices were expected to remain elevated in the short-term, they were projected to fall as demand/supply imbalances in the global economy improved.

- The risks to the inflation forecast are skewed to the upside and these risks have intensified. Upside risks (which means that inflation could track above the forecast) include higher than expected inflation expectations stemming from the shock to international commodity and shipping prices, a higher than projected pass through of the increases in these international commodity and shipping prices to domestic prices and the impact of recent storms on the supply of agricultural foods and their prices. Of note, the fall in international grains prices to date have been stronger than expected but the effects of this are not likely to offset the impact on domestic inflation of the other shocks.

While the risks to the forecast for energy-related prices are skewed to the upside, the risks to grains prices are skewed to the downside. Oil prices trended below the Bank’s forecast during August 2021, due to lower fuel demand amid the spread of infections and an appreciation of the US dollar. However, LNG prices trended above the forecast over the month amid warmer-than-usual temperatures in the US and expectations for colder winter temperatures. International grains prices trended below the Bank’s projections in the context of increased production and expectations for slower demand growth in China.

- An assessment of the risks to the domestic GDP growth forecast suggests that GDP growth is still likely to fall within the range of 7.0 per cent to 10.0 per cent for FY2021/22 but this is now likely to be closer to the lower end of the forecast range. Economic activity is now expected to be affected by weaker than anticipated global growth, a temporary disruption to production at one of Jamaica’s main alumina plants, tightened COVID-19 measures and adverse weather. In this context, growth in Mining & Quarrying, Agriculture, Forestry & Fishing and other sectors are expected to be weaker than previously anticipated. Notwithstanding, the economy is still expected to continue to grow from the June 2021 quarter onwards and return to pre-COVID-19 levels by the end of 2022. The principal downside risk to GDP growth over the forecast horizon is the continued adverse impact of the novel coronavirus on the Jamaican economy.

- GDP growth in the US is also likely to be lower than projected mainly due to the spread of the Delta variant, the measures taken to control its spread and constraints posed by the shortage of key raw materials. Notwithstanding, economic activity in the US continues to be aided by the progressive control of the COVID-19 pandemic in the context of vaccine rollouts and the release of pent-up demand. Inflation in the US decelerated to 5.3 per cent at August 2021, above the target of 2.0 per cent, and is projected to remain elevated for some time.

- The domestic fiscal policy stance continues to pose no risk to inflation over the near term.

The MPC will continue to closely monitor the economic environment and is prepared to take further action at the next MPC meeting to achieve its objective."

0 comments:

Post a Comment